Resetting the relationship between local and national government. Read our Local Government White Paper

Navigating financial uncertainty and building resilience: Guiding principles

The local government sector has been grappling with sustained financial pressures since 2010, encountering a myriad challenges that complicate the task of budgeting and planning for the medium-term. This guide focuses on helping local authorities’ finance functions to plan and manage in these challenging times.

Introduction

a. Purpose of the guide

The local government sector has been grappling with sustained financial pressures since 2010. This guide focuses on helping local authorities’ finance functions to plan and manage in these challenging times, encountering a myriad challenges that complicate the task of budgeting and planning for the medium-term. Recently, these financial challenges have heightened, further complicating a local authority’s ability to present a balanced budget without the use of reserves and placing additional strain on the finance function as well as wider service teams. Where this guide refers to the “finance function” we mean all finance officers that are supporting financial management processes.

Amidst this level of uncertainty, it can seem that trying to plan is a futile exercise. However, during periods of uncertainty, good practice in financial planning becomes more important and urgent than ever. It is important for the finance function to help change the approach and mindset of the organisation when dealing with uncertainty, ensuring that solutions for mitigating and managing financial risk are identified. This guidance identifies strategies and principles for the finance function to promote such an approach, identifying ways of working and behaviours that can be adopted.

In response to this escalating financial uncertainty, this guide is designed to equip chief executives, Section 151 Officers and their respective teams with practical advice, guidance, and tools that can be effectively implemented to improve financial resilience. The guide is specifically focussed on helping local authorities comprehend, articulate, and manage some of their most pressing issues.

While the implementation of the principles outlined in the guide cannot eliminate financial uncertainty, their proper application can offer early identification of key risk areas. Additionally, improved mitigation and communication of issues will aid decision-makers in navigating through the most challenging financial decisions.

b. How it has been developed

This guide is a collaborative effort between the Local Government Association (LGA) and EY’s Local Government Practice. In the process of its development, we actively sought insights from Section 151 Officers across the country, aiming to grasp the prevailing uncertainties they confront and identify leading practices for managing financial uncertainty. Additionally, to refine the guide's focus, we facilitated a series of roundtable discussions to help ensure that the guide not only addresses key issues, but also provides practical and actionable tools that can be readily developed and applied.

c. Fiscal, economic, and service uncertainties

Financial uncertainty in local government is driven by a multitude of factors. Local authorities’ ability to mitigate the funding and demand pressures they face has been impacted by a financial framework characterised by one-year funding settlements and minimal funding reforms. Local authorities need greater certainty on funding through multi-year settlements and more clarity on financial reform so they can plan effectively and maximise the impact of their spending over the medium-term. Concurrently, local authorities are experiencing unprecedented demand for vital services such as social care, Special Educational Needs and Disability (SEND) and homelessness, which further exacerbate the financial strain faced by local authorities. Rising inflation, surging energy costs, and increasing pressures such as the national living wage place additional burdens on local authority budgets. Recent unforeseen events like the Covid-19 pandemic and the cost of living crisis exemplify incidents that have resulted in unexpected financial burdens for the sector.

d. Navigating financial uncertainty

In the face of an evolving local government financial landscape, authorities are required to be more efficient than ever in navigating uncertainty. Achieving this requires a comprehensive and proactive approach to financial management. To tackle financial uncertainty, local authorities must engage in vigilant financial planning, incorporating robust risk assessment procedures, implementing effective governance structures and fostering open communication and engagement among all stakeholders. Risk management strategies should be integrated into every level of financial planning and involve regular scenario forecasting and stress testing to develop agile responses. The capacity of local government to navigate financial uncertainty relies upon the adoption of strategic financial and risk management practices across the local authority, and is not just the work of the Section 151 Officer and the finance function. It needs to be embedded into the foundation of the organisation and form part of the governance and structure to provide appropriate oversight and accountability.

e. How to use this guide

This guide is designed to aid local authorities in navigating the various challenges contributing to financial uncertainty. While it is not anticipated that users implement the entire checklist, this guidance offers a nuanced approach distinct from financial management advice by emphasising the specific tools to assist in addressing financial uncertainty and to support the delivery of the Section 151 Officer’s statutory functions.

The significant financial challenges which local authorities are dealing with can limit capacity to optimise their approaches to dealing with those challenges. Whilst this guidance presents tools and solutions that are not resource-intensive, it is not essential to adopt every recommendation and even incremental steps can make a difference. Using the checklist as a tool for self-assessment can help all authorities consider where there is potential to make improvements, however small, to their approaches to navigating financial uncertainty.

The report is structured around five key sections, aligned to the areas where focus should be applied to navigate financial uncertainty, as follows:

- Section 1 – Strategic financial planning

- Section 2 – Empowering finance functions

- Section 3 – Strengthening financial stability

- Section 4 – Developing economic stability and sustainable local growth

- Section 5 – Strategising risk

Each section then comprises:

- Principles – The proposed standards and areas of focus that support the navigation of financial uncertainty; and

- Actions – The tools and approaches that can enable the implementation of the proposed principles.

Where other available guidance relevant to the sector is relevant to the principles, this has been signposted accordingly.

Appendix 1 includes a checklist that can be used by a local authority to undertake a self-assessment to identify gaps and areas of improvements based on this guide. After implementing actions from this guidance, a reflective review could be undertaken to determine the effectiveness of the measures implemented, assess progress and explore areas for further improvement.

Section 1: Strategic financial planning

Whilst the financial planning process culminates with the submission of budget papers to Cabinet in February/March, effective financial planning, especially during periods of uncertainty, demands a continuous, year-round approach. Assumptions must be consistently refined and challenged as new information becomes available. Despite the common perception that budget development is primarily a finance-driven activity, with the finance function taking the lead, it is crucial to recognise that a collaborative approach between the finance function and services is essential to mitigating uncertainty. Service managers should play a pivotal role in driving the process, working alongside the finance function to plan for and deliver a balanced budget.

To navigate financial uncertainty, three key principles have been identified that must be diligently undertaken in the financial planning process. These principles aim to enhance strategic financial planning, establishing a robust foundation to deal with financial uncertainty.

| Key principle | Guidance notes |

|---|---|

| 1.Local authorities must ensure that the budgeting process is an integral component of corporate and service planning processes. | Principle 1.1: Supporting strategic decision making through effective horizon scanning, scenario planning and financial forecasting. |

| 2. Local authorities must ensure that the financial planning process is realistic, balancing ambition and reality to develop implementable budgets. | Principle 1.2: Aligning financial strategy with the corporate plan to maintain synergy. |

| 3. As part of the financial planning process, horizon scanning and scenario planning should be undertaken to identify areas of uncertainty. | Principle 1.3: Balancing ambition with practicality to ensure successful implementation in challenging conditions. |

Principle 1.1: Supporting strategic decision making through effective horizon scanning, scenario planning and financial forecasting

Horizon scanning, scenario planning, and financial forecasting are all tools that allow local authorities to anticipate potential risks, challenges, and opportunities during periods of uncertainty, thus guiding corresponding strategic decisions and actions. These tools can equip decision-makers with the ability to be proactive amidst a changing and volatile financial landscape, supporting resilience of a local authority in the face of unexpected circumstances or changes in the fiscal environment.

Principle 1.2: Aligning financial strategy with the corporate plan to maintain synergy

The need to model and manage uncertainty should be balanced with the policy aspirations of the local authority. To maintain this dynamic link, it is crucial to align any corporate or service planning processes within the medium-term budgeting process.

Without this, there is a risk is that the medium-term financial plan is not relevant to corporate planning. In periods of uncertainty, it is vital to ensure that there is a consistent and well-understood direction of travel for the local authority, with strategic decisions across service provision and finance being made in tandem. The synchronisation of these timelines helps ensure that neither exercise is completed in isolation of the other. Integrating financial planning with overall strategic planning will ensure a cohesive approach towards achieving the organisation's objectives and enable a well-balanced allocation of resources in line with strategic priorities.

The intention is to create a continuous loop of strategic input, financial planning, delivery, and monitoring, thus strengthening both the financial strategy and the corporate plan. By fostering a robust connection between financial considerations and strategic planning, this alignment positions service managers to manage their financial responsibilities proactively and responsively, driving the local authority’s resilience in the face of financial uncertainty.

Outlined below are three key actions that a local authority can take to help align the financial strategy with the corporate planning process.

Principle 1.3: Balancing ambition with practicality to ensure successful implementation in challenging conditions

Realistic budgeting plays a vital role in a local authority’s financial management, particularly when helping to navigate financial uncertainty. When budgets are practical and match reality, it allows the finance function to allocate resources accordingly, reacting to in year challenges in a responsive and dynamic manner. By incorporating a pragmatic view of income, expenditure, and financial reserves, realistic budgets provide a solid foundation for strategic financial decision-making, improving the local authority’s overall financial resilience.

Realistic budgeting can significantly enhance financial planning and control mechanisms within a local authority. Budgets that accurately reflect the local authority’s financial potential and constraints enable a meaningful and informed analysis of financial performance. This allows the finance function to closely monitor income and spending against planned budgets, identify any deviations promptly, and make necessary adjustments. Continuous adjustment and alignment of budgets with the actual financial environment contribute to better risk management, thus enabling the local authority to navigate financial uncertainties more effectively.

The following outlines three key actions a local authority can take to bolster the realism in their budget planning process, helping to bridge the gap between ambition and practicality.

Section 2: Empowering finance functions

In an ever more complicated, challenging and uncertain fiscal and economic environment, effective financial stewardship and risk management requires a finance function which is fit-for-purpose. A finance function, armed with the right skills, knowledge, tools and authority, is well-positioned to pinpoint key areas of financial risk and uncertainty across the local authority, and to devise proactive strategies to mitigate them effectively.

A strong performing finance function relies upon:

- The skills and capabilities of its finance teams;

- The relationship it holds with the organisation, to foster an open environment to address risks as well as to provide clarity on the roles, expectations and lines of accountability; and

- How it (and the wider organisation) is enabled by technology so that stakeholders have access to information to support financial management and can focus on complex, value add activities.

To help build a dynamic finance function, that is focussed on driving financial resilience across the local authority, three strategic principles have been identified, which are supported by actions.

| Key principle | Guidance notes |

|---|---|

| 1. Local authorities must have an appropriately skilled and proficient finance function that can set the tone for financial stewardship. | Principle 2.1: Being proactive and engaged as a finance team. |

| 2. Corporate objectives should encourage collaboration and cooperative efforts across departments. | Principle 2.2: Ensuring effective relationships are built between the finance function and services. |

| 3. Embrace technology as a catalyst for enhancing efficiency across the local authority. | Principle 2.3: Using technology to enable financial stewardship. |

Principle 2.1: Being proactive and engaged as a finance team

There is a shortage of local government accountants and finance officers across the sector, with most areas of the country struggling to attract the appropriate skillsets. Creating and maintaining an engaged and proactive finance function is a key part of talent attraction and retention.

The culture of the finance function also sets the tone for financial stewardship across the organisation. To foster a proactive and engaged finance function, this guide proposes strategic actions for local authorities to implement.

Principle 2.2: Ensuring effective relationships are built between the finance function and services.

Building effective relationships within the finance function, with service managers, elected members and external stakeholders, is crucial for fostering a collaborative working environment, where financial uncertainty is regularly communicated and discussed. Open and transparent relationships built on trust, promote an environment where risks can be surfaced and managed swiftly and comprehensively. It is important for the finance function to be viewed as trusted professional advisors across the organisation, rather than as a blocker or hurdle.

An open dialogue about financial uncertainties and potential risks allows the finance function to provide timely advice and insights that inform decision-making processes in service departments. This trust-based environment encourages service heads to engage directly in financial discussions, promoting a culture of accountability and active participation in budget management. Two-way communication supports service departments to build effective service plans within the budget envelope provided and understand any budget changes. Fostering the culture of trust and open communication within the organisation encourages pre-emptive risk management, leading to the creation of more accurate and sustainable budgets.

Principle 2.3: Using technology to enable financial stewardship.

Technology can support financial stewardship by:

- Creating capacity so that staff focus on more strategic tasks instead of time-consuming administrative work.

- Utilising more extensive datasets to support more proactive and informed decision making.

Outlined below is guidance on how best to deliver against these actions.

Section 3: Strengthening financial stability

Building financial resilience is crucial for ensuring the long-term sustainability of local authorities. Through maintaining strong balance sheets, local authorities display their ability to withstand financial uncertainty and fulfil community commitments. It is important that the local authority ensures that liabilities are sustainably managed, but also that local authority assets support key local authority objectives and wider community prosperity. Investing in the right capital programmes has not only the potential to improve the quality of local community life, but also to provide valuable collateral for securing finances and help bolster balance sheet resilience.

To help build long-term financial sustainability, three key principles have been outlined, which local authorities should aspire to deliver.

| Key principle | Guidance notes |

|---|---|

| 1. Building resilience within the balance sheet for long-term sustainability. | Principle 3.1: Building balance sheet resilience. |

| 2. Maintaining control over capital activities and assets for financial stability, risk avoidance and sustainable growth. | Principle 3.2: Ensuring grip over capital activity and assets. |

| 3. Ensuring investment decisions align with the long-term growth and financial stability of the local authority. | Principle 3.3: Managing investment risk. |

Principle 3.1: Building balance sheet resilience

Balance sheet resilience is crucial for a local authority in the face of financial uncertainty as it acts as a financial buffer, supporting the local authority’s ability to maintain critical services even during unexpected financial downturns. A resilient balance sheet, characterised by strong assets and resilient and sustainable servicing of liabilities, signifies financial health and stability, providing the local authority with a solid foundation to navigate uncertainties and continue delivering its vital services to the communities it serves.

Principle 3.2: Ensuring grip over capital activity and assets

Amid increasing financial uncertainties, this principle provides tools, strategies and measures to maintain firm control over capital activities and assets. It outlines the importance of proactive asset management, developing robust capital strategies and the need to undertake agile capital viability assessments. The aim is to enhance financial resilience by ensuring efficient handling of capital assets that would otherwise be exposed to uncertainty.

Principle 3.3: Managing investment risk

Managing investment risk is a key concern for local authorities amidst ongoing financial uncertainty. A proactive, well-calibrated approach to managing investment risk is necessary, especially in the current financially volatile landscape. How local authorities respond to these risks can significantly impact financial stability and the continued provision of essential public services. This section provides insights, strategies, and best practice to help navigate investment risk, protect public funds, and support the sustainability of service operations.

Section 4: Developing economic stability and sustainable local growth

In an unstable fiscal environment, local authorities can improve their longer-term financial resilience and build certainty by understanding, engaging with and helping to build the local economy and local supply markets.

The role of the finance function plays an important role in helping to build a sustainable local economy and supply chain, via:

- The financial planning support it provides to the local authority to meet its local economic growth objectives; and

- Its strategy to safeguard resources through working alongside services to undertake active demand management.

The finance function needs to work with colleagues with economic development, commissioning and supporting workforce specialisms to understand the interplay between these activities and financial management. These areas of activity are a source of greater uncertainty if they are not adequately understood.

The three key principles underpinning these are as follows:

| Key principle | Guidance notes |

|---|---|

| 1. Strong local economic growth can help secure financial certainty and reduce reliance on central government. | Principle 4.1: Developing place-based growth strategies to secure long-term economic prosperity. |

| 2. Proactively managing demand enables early intervention for long-term sustainability. | Principle 4.2: Identifying opportunities to manage demand. |

| 3. Managing supply can achieve a better outlook if combined with appropriate workforce strategies. | Principle 4.3: Cultivating resilience and sustainability in local supply chains. |

Principle 4.1: Developing place-based growth strategies to secure long-term economic prosperity

Whilst they can never fully answer the need for adequate funding from national government, place-based growth strategies can contribute to a local authority's long-term financial resilience and sustainability by focusing on the unique potential and opportunities within a specific locality. These strategies leverage local assets, strengths, and resources to stimulate economic growth and development which benefits the local population. The role of the finance function is to collaborate with place-based services which are working through partnerships with other organisations invested in the local area to develop a targeted a place-based growth strategy, in a manner that contributes to financial resilience and sustainability.

By driving local economic growth, local authorities can increase their own revenue streams through means such as council tax or business rates, leading to a stronger and more sustainable financial position as well as improving community resilience, prosperity and wellbeing. This approach also creates local jobs, reduces unemployment expenses, and can stimulate further investment in the area.

In short, place-based growth strategies enable local authorities to build on unique local characteristics to spur economic growth, strengthening their financial position, and fostering overall sustainability. By nurturing local growth, local authorities equip themselves to weather financial uncertainties while simultaneously contributing to the wellbeing of the community they serve.

The finance function plays a vital role in the development of place-based growth strategies, primarily by integrating the potential implications and outcomes into the financial planning process. Whenever additional growth is anticipated, it is crucial for the finance function to construct well-informed assumptions about the potential influence of this growth on the local authority’s financial standing. This includes, but is not limited to, estimating impacts on tax revenue and changes in service demand. Highlighted below are two primary actions that the finance function should undertake to effectively support these strategies.

Principle 4.2: Identifying opportunities to manage demand

Identifying opportunities to manage demand is a critical measure in navigating financial uncertainty effectively. The ability to balance the demand for services with available resources allows local authorities to operate within their means while still meeting the needs of their residents. Proactively identifying these opportunities, such as alternative service delivery models, building capacity within service users and the community or place-based schemes that promote self-reliance, helps make service provision more sustainable. It reduces reliance on local authority services, thus directly impacting the local authority’s financial standing by potentially freeing up resources for other crucial endeavours or investment.

The finance function holds a pivotal role in supporting services to identify demand management strategies, illustrating how these strategies contribute to mitigating long-term financial pressures. By helping to develop a solid evidence base, they demonstrate how proactive investment and intervention can decrease future service demand. The finance function will need to demonstrate analytical skills to forensically understand the cost drivers of demand in respective services, and then work in collaboration with services to understand the feasibility of demand management initiatives and how they will be tracked to measure performance.

Principle 4.3: Cultivate resilience and sustainability in local supply chains

Building resilient supply chains in local authorities often involves ensuring the sustainability of local markets. The focus, in this case, is on creating an environment where firms are incentivised to grow and diversify their offerings in the local area. This approach reduces the market's dependence on a few suppliers, thereby promoting competition, increasing consumer choices and enhancing the overall stability and resilience of the local supply chain.

Take, for instance, care markets. These are vital for the local authority’s provision of health and social care services. A sustainable care market would feature a diverse range of providers offering various services, from home care to residential care, respite care and more. To achieve this, local authorities can take a proactive role in market shaping, using mechanisms such as commissioning strategies, fair pricing, and communication strategies to incentivise provider growth and diversification.

Promoting local growth and supporting local suppliers in these markets is vital, as this contributes to market sustainability, helps manage risks associated with external suppliers, and strengthens the local economy. At the same time, local authorities must maintain up-to-date contingency plans to mitigate potential disruptions in care provision.

Through these measures, local authorities can help build market sustainability. This not only ensures continuity of crucial services like care provision but also contributes to the local authority’s long-term financial resilience, safeguards their operations, and supports the wellbeing of the community.

In developing resilient supply chains within local authorities, the finance function holds a critical role to inform decisions that foster a sustainable local market. They help in shaping commissioning strategies and in determining fair pricing mechanisms that incentivise providers to diversify their offerings. By analysing financial data and market trends, they support services to identify opportunities for local growth and help manage risks associated with external suppliers. The finance function assists the safeguarding of operations and contributing to the local economy's resilience and sustainability.

Section 5: Strategising risk

An effective risk framework is vital to local authorities as it supports the continuity of services by identifying and preparing for potential risks, and their corresponding financial impact should they materialise. Moreover, such an approach significantly aids the development of effective mitigations during periods of financial uncertainty, supports the effective use of resources, and is essential in demonstrating good governance and a commitment to accountability. This also supports informed decision-making, balancing benefits against potential risks. A risk-focused culture embedded by senior leaders throughout the local authority ensures that all staff are acute to risk warnings and can take swift pre-emptive measures against them.

Several local authorities have found themselves in a position where they have had to issue a section 114 notice, which indicates serious financial difficulties. It could be argued that this situation has partly occurred due to the approach these authorities have taken towards managing risk, along with the level of risk they have been prepared to accept within their organisation. To be effective, risk management must be seen as an integral part of governance and strategic planning rather than a stand-alone activity. The three principles within this section will help you to build a robust risk framework.

| Key principle | Guidance notes |

|---|---|

|

Principle 5.1: Ensuring that risk is effectively identified and assessed. |

|

Principle 5.2: Developing plans to manage and monitor risk. |

|

Principle 5.3: Using contingencies and reserves to manage risk. |

Principle 5.1: Ensuring that risk is effectively identified and assessed

A proactive approach to risk identification allows local authorities to anticipate issues and mitigate against them, as opposed to a reactive approach, which can result in higher costs and is less viable in periods of uncertainty. Once a risk is identified, it is important to monitor variations in the threat level and developments that could introduce further financial pressure for the local authority. Where risk levels increase significantly, decisions should be revisited, or at the least decision makers should be informed.

Principle 5.2: Developing plans to manage and monitor risk

This segment outlines the pivotal actions a local authority should undertake to control and scrutinise risks and deploy comprehensive scenario planning that bolsters the credibility of assumptions adopted in the Medium-Term Financial Strategy (MTFS). This includes ensuring risk management is supplemented with an open and well-defined governance and control system for effective review, supervision and monitoring.

Collaboration with Internal Audit can ensure that the audit plan focuses on the areas within the organisation where strategic risks are prevalent, considers whether appropriate measures are in place to manage risk and reviews progress made.

Principle 5.3: Using contingencies and reserves to manage risk

Effective risk management can reduce the call on reserves and the need to hold them, but there will always be a need for reserves and contingencies in local authority finances because some things are inherently uncertain and defy risk management interventions.

This involves planning for both expected and unexpected outcomes and includes the consideration of the requirement for contingencies and reserves to manage risks should they materialise. The challenge for the sector is having dwindling levels of reserves and contingencies to respond to risks, given challenges about resourcing and the multitude of factors impacting the financial stability of a local authority. As a result, contingencies and reserves should be utilised carefully, whilst longer term funding is identified.

Appendix

Checklist

| Section 1: Strategic financial planning | |

| 1.1 Supporting strategic decision making through effective horizon scanning, scenario planning and financial forecasting | |

| Action | Tool |

| 1.1a Ensure various sensitivities and scenarios are considered as part of the financial planning process | Financial Management Code (CIPFA) |

| 1.1b Build and use a suite of financial models to run these scenarios and capture the key assumptions utilised | The Annual Budget Process (Must Know Guide, LGA) |

| 1.1c Understand the availability and appropriateness of external and internal data and utilise it for financial modelling | Guidance on using different sources of data |

| 1.2 Aligning financial strategy with the corporate plan to maintain synergy | |

| Action | Tool |

| 1.2a Align timelines for key service planning milestones with financial planning processes to ensure they are consistent | |

| 1.2b Create a culture where all staff understand corporate priorities and use them to guide the budgeting process | The role of the CFO in public service organisations (CIPFA) |

| 1.2c Develop an environment of clear and consistent communication and engagement, which sets clear strategic direction on the financial planning process |

Financial Management Code (CIPFA)

Finance communication and engagement approach |

| 1.3 Balancing ambition with practicality to ensure successful implementation in challenging conditions | |

| Action | Tool |

| 1.3a Encourage an understanding and effective communication of budgetary trade-offs across the local authority to facilitate strategic decisions that balance ambition and practicality | Steps on navigating trade-offs |

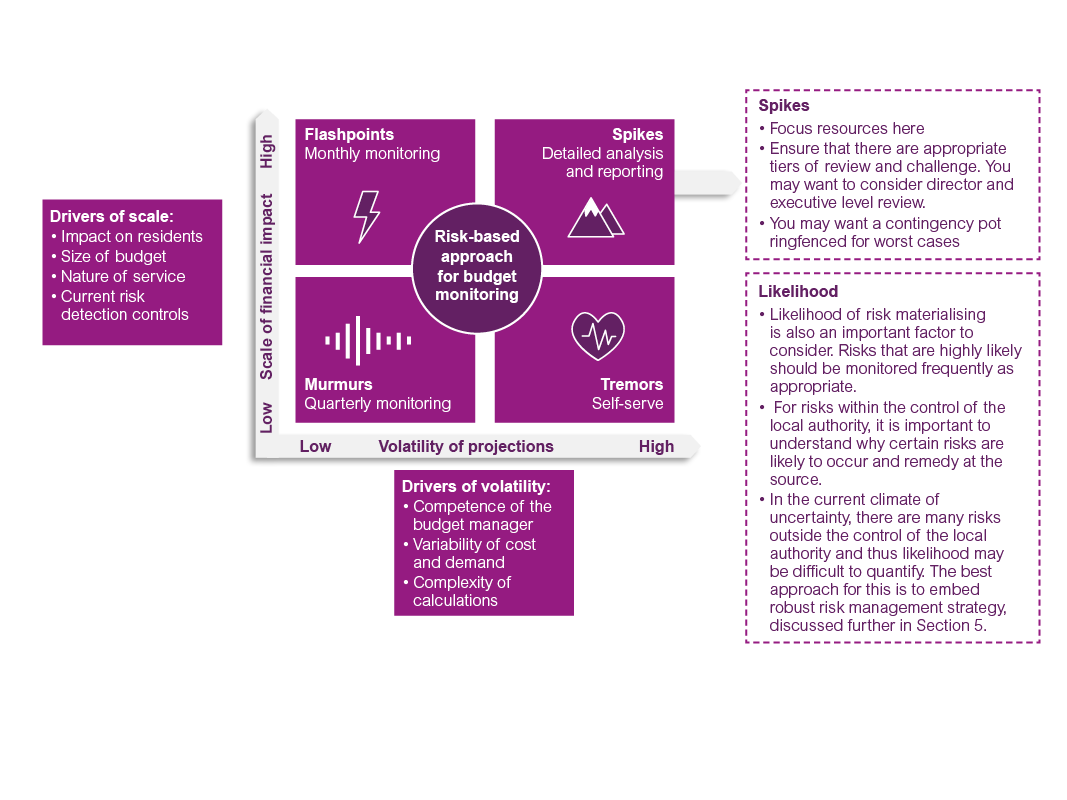

| 1.3b Refine the budget monitoring process by adopting a risk-based approach | Matrix for a risk-based budget monitoring process |

| 1.3c Ensure a collaborative approach between the finance function and services during the budgeting process | Key questions for finance to consider to help foster a collaborative budgeting approach |

| Section 2: Empowering finance functions | |

| 2.1 Being proactive and engaged as a finance team | |

| Action | Tool |

| 2.1a Baseline your finance function to understand the gaps in capability & capacity and to create an action plan to bridge the skills deficit |

Baseline workforce maturity index

|

| 2.1b Develop an attractive employee offer to attract, develop and retain talent | Workforce planning(LGA), Workforce capacity (LGA) and Recruitment and retention best practice (LGA) |

| 2.2 Ensuring effective relationships are built between the finance function and services | |

| Action | Tool |

| 2.2a Define the role and responsibilities of finance and budget holders through training and shared service objectives | Financial Management Code (CIPFA) |

| 2.3 Using technology to enable financial stewardship | |

| Action | Tool |

| 2.3a Automate business processes and improve operational efficiency and the control environment |

Framework for improving the control environment

|

| 2.3b Enable budget managers to proactively own and manage their budgets |

Financial Management Code (CIPFA)

Key questions for identifying whether a budget manager can actively manage their budget |

| Section 3: Strengthening financial stability | |

| 3.1 Building balance sheet resilience | |

| Action | Tool |

| 3.1a Develop a reserve structure/strategy | Developing key components of a reserve management strategy |

| 3.1b Undertake Balance Sheet reporting | |

| 3.1c Model the impact of decisions on cash, MRP and capital financing | |

| 3.2 Ensuring grip over capital activity and assets | |

| 3.2a Undertake proactive asset management | Asset management plan framework and policy |

| 3.2b Develop robust capital strategies underpinned by detailed, scenario supported, forecasting | Components of a capital strategy |

| 3.2c Foster agile capital viability assessments | |

| 3.3 Managing investment risk | |

| Action | Tool |

| 3.3a Adoption of a robust investment strategy and financial framework | Investment Financial Framework |

| 3.3b Ensure non-financial contributions to operations, communities and services | |

| Section 4: Developing economic stability and sustainable local growth | |

| 4.1 Developing place-based growth strategies to secure long-term economic prosperity | |

| Action | Tool |

| 4.1a Support the delivery of economic development objectives with financial planning | How the finance function support to promote local growth |

| 4.1b Identify place-based schemes to support residents and reduce service dependence | Key roles for the finance function |

| 4.2 Identifying opportunities to manage demand | |

| Action | Tool |

| 4.2a Provide evidence to inform planning of preventative services that help reduce demand for statutory services | Steps for the evidencing the need for investment in preventative services |

| 4.2b Support services to identify demand management strategies across the local authority | Actions for the finance function to help manage demand |

| 4.2c Support the development of associated saving plans and business cases | Financial Management Code (CIPFA) |

| 4.3 Cultivating resilience and sustainability in local supply chains | |

| Action | Tool |

| 4.3a Undertake analysis to identify supply chain resilience issues | |

| 4.3b Contribute to the development of market sustainability plans | Key steps for the development of market sustainability plans |

| 4.3c Provide support for the development of workforce strategies for attracting, retaining and developing local talent | Considerations for an effective workforce strategy |

| Section 5: Strategising risk | |

| 5.1 Ensuring that risk is effectively identified and assessed | |

| Action | Tool |

| 5.1a Develop a comprehensive risk management framework | Key roles for the finance function |

| 5.1b Develop a comprehensive risk assessment methodology that considers multiple sources of risk (both internal and external to the local authority) | Methodology for risk assessment |

| 5.1c Work collaboratively with services and internal audit to assess the likelihood, impact and quantify the associated financial risk | Essentials for successful collaboration under your risk strategy |

| 5.2 Developing plans to manage and monitor risk | |

| Action | Tool |

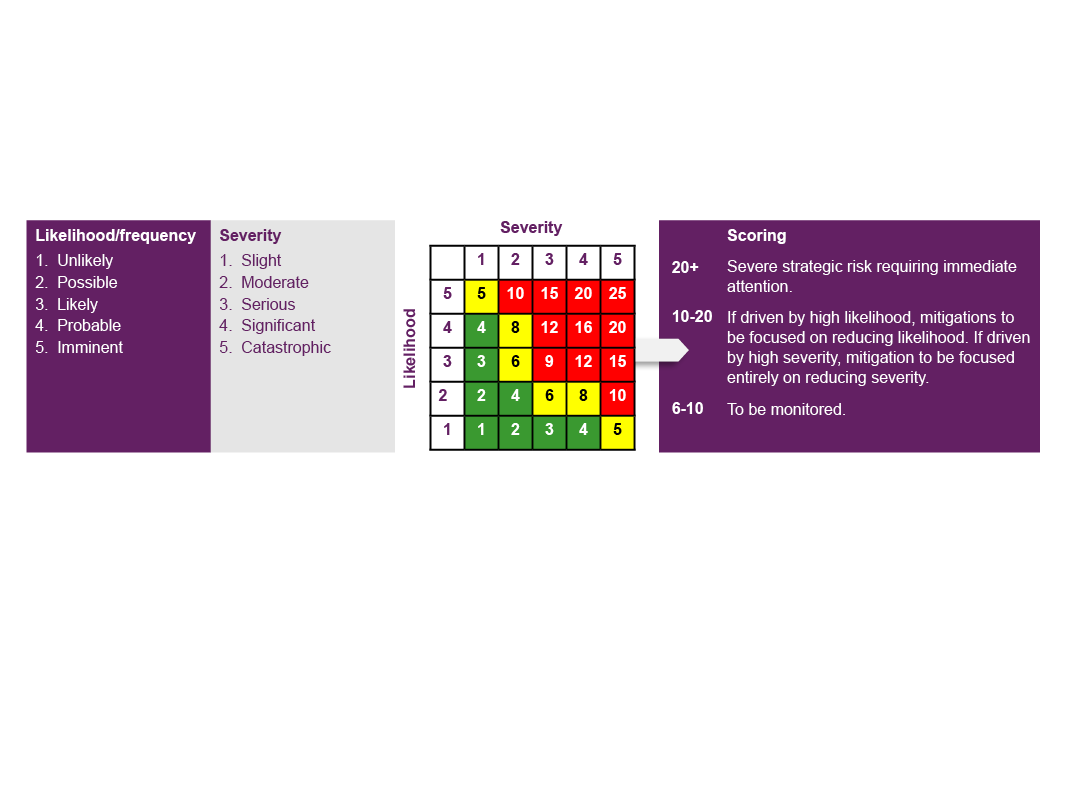

| 5.2a Undertake robust scenario planning considering the likelihood and quantification of risks should they materialise |

Risk assessment best practice

|

| 5.2b Have clear and transparent governance mechanisms to oversee risk management | |

| 5.3 Using contingencies and reserves to manage risk | |

| Action | Tool |

| 5.3a Establish robust contingency funds to address unexpected fiscal challenges | Components to consider when utilising contingencies and reserves |