Resetting the relationship between local and national government. Read our Local Government White Paper

Improvement and assurance framework for local government

Each council must take appropriate measures to gain assurance both of the performance of its services and of its corporate governance. This framework is designed to support local authorities to understand the various components of assurance and accountability in local government, and to access guidance and support to increase the effectiveness of assurance activities in the sector.

Introduction

Councils are responsible for their own performance and improvement. This is recognised in the ‘sector-led improvement’ approach which is underpinned by the key principles that councils:

- are primarily accountable locally, not nationally;

- have a sense of collective responsibility for the performance of the local government sector.

- The LGA’s role is to provide tools and support councils and also to maintain an overview of the performance of the sector

In order to comply with the best value duty to secure continuous improvement in the way the authority’s functions are exercised, each council must take appropriate measures to gain assurance both of the performance of its services and of its corporate governance. Through a focus on effective assurance, councils can mitigate the risks and costs of failure and their impacts on local residents and businesses.

There has not previously been a document or framework which sets out, in one place, the various required components of local government assurance, how they all fit together, how to use them effectively and what improvement support is available to help. This framework aims to:

- support councils to understand how to use the components within the framework and how they fit together;

- increase the effectiveness of assurance in the sector. While it cannot itself prevent failures, its use may reduce the risk – and costs - of statutory or non-statutory intervention, whether by Oflog, central government or other regulators;

- make it easier for local residents and businesses to understand how to hold their local authority to account.

Assurance may sometimes be seen as a dry topic, and accountability may, wrongly, be feared. However, the management and routine operation of internal controls and risk management support councils to manage the future constructively and safely. As one council leader said, ‘it’s what helps me to sleep at night’.

It is not just the responsibility of the monitoring officer or the head of internal audit. All members have a responsibility to oversee effective governance, and all officers have a duty to comply with good governance and provide information to demonstrate that compliance.

Assurance cannot be gained ‘by numbers’ or a one-off event: there is no simple list of yes/ no indicators which will help a council decide whether or not it can be assured of its performance or governance. It is achieved through a series of nuanced, qualitative judgements, often informed by assessments of behaviours and relationships. It is essential to triangulate numerous sources of evidence, and to apply multiple assurance activities effectively, to gain a view of the council in the round.

Not all of the components of the system are currently working as well as they should. In the context of continuing crisis in local audit, it is more important than ever that councils should undertake their own assurance activities effectively. The LGA will continue to work with its partners to seek to ensure continuous improvement of the system and all of its components.

Elected members play a crucial and continuous role in seeking assurance of the council’s activities and governance. This includes assurance of each council’s own local objectives, for which they are accountable to their local electorate. Councils will rightly make political choices in response to local circumstances: successful authorities make these choices within the context of good management practice, consideration of cost-effectiveness and value for money, robust controls and risk management.

Councils exist to improve the quality of life of, and the quality of places for, the communities they serve. Therefore, the focus of councils’ assurance work is on the assurance they provide to local communities.

This framework includes the ‘nuts and bolts’ – the key components of local authority assurance. Many of these are processes and structures. The framework also includes organisational culture, behaviours and ways of working, since constructive working relationships are fundamental to effective assurance activities. There is a crucial role for political and managerial leaders in challenging poor behaviour (in both formal and informal settings) and non-compliance.

It will not always be possible for assurance to be gained, particularly as the scale of challenges facing local government increase. Where positive assurance is not possible there is support available – from the LGA and from others in the sector – to help the council put things right. By using the assurance system and its components effectively, councils can increase their chances of identifying issues and addressing them before they get more difficult – and costly – to fix. The cost of statutory intervention can be far greater than the cost of sector support.

Sector-led improvement has always played a part in providing councils with assurance of their own performance. Increasingly, it contributes to the assurance of councils' performance for the wider public and central government. The LGA will work with professional bodies to maintain an overview of the sector’s performance, seeking to ensure that support is targeted where it is needed.

What is the scope and status of this framework?

The framework is applicable to unitary, county, district and borough councils in England, and to English authorities with all types of governance system. The specific assurance requirements for combined authorities are set out in the English Devolution Assurance Framework but the principles in this framework will apply to combined authorities too.

The framework is part of a suite of guidance, tools and resources for the sector produced by the LGA and other bodies. Effective assurance is achieved mainly through the application of best practice rather than statutory activity, although the framework points to statutory provisions where relevant.

Failure in one service area may impact significantly on the whole organisation. Since the scope and objectives of the local government sector are so wide-ranging, this framework is mainly focused on corporate areas and overarching governance, rather than including every service-specific source of assurance. Each service area will have its own mechanisms for assurance and accountability and councils will need to assure themselves of compliance with statutory duties in each case. Effective corporate assurance will support assurance of individual services and the principles and good practice identified in this framework will apply to all services as well as corporate activities.

What is the relationship between this framework, corporate peer challenge, best value standards, Oflog and statutory interventions?

At any one time, each local authority will be at a point on a continuum. At one end are authorities which have a strong awareness of their strengths and areas for development, are proactive in seeking opportunities for improvement and delivering best value (even where performance is strong) and elected members and officers take appropriate actions to assure themselves in relation to their performance and governance.

The characteristics of a well-functioning authority set out in the best value standards include effective use of many of the framework’s components: equally, the standards’ indicators of potential failure may arise where assurance activity is not effective. A failure to deliver best value is, essentially, a failure of governance. Achieving continuous improvement requires an ongoing drive to move from ‘good’ to ‘great’.

At the other end, a small minority of authorities are not sufficiently self-aware, do not take effective action to achieve continuous improvement, do not have effective assurance arrangements and consequently have entered statutory intervention. Local authorities can and do move between points on this continuum over time.

The LGA works with professional bodies, regional groupings of councils, and others to support as many local authorities as possible to stay at the positive end of the continuum, aiming to prevent authorities from moving towards the ‘intervention’ end, so that they continue their improvement journey even further. The LGA’s corporate peer challenge is one of the improvement tools that councils can use as part of their assurance of their own performance and governance, so that they can address their own challenges where possible without central government (including Oflog) or regulators needing to become involved.

How was this framework developed?

The LGA has consulted with local authorities, professional bodies and other key stakeholders to prepare this framework and supporting guidance, which has been informed by draft guidance on best value standards and intervention and learning from recent council failures. We also had helpful discussions with commissioners and Oflog. CIPFA, Lawyers in Local Government and Solace acted as a ‘sounding board’ during the drafting process.

Developing the framework has been an iterative process and the LGA will continue to develop it over time as new insights and best practice are identified, reviewing the framework at least annually. Tools and training to support its implementation will also be developed by the LGA and partners.

What do we mean by assurance?

We have developed the following definition through consultation with the sector:

Timely and accurate information, evidence and evaluation of how local authorities are delivering their duties, functions and outcomes, which can be used to hold them to account and may give confidence.

There should be no assumption that assurance will always be gained – in some cases the outcome will be ‘not assured’.

A ‘not assured’ outcome – as long as it is acted upon – may be as valuable to an authority as ‘assured’.

How does accountability work?

The Review of Audit and Accountability defined accountability as...

…the requirement to provide explanations about the stewardship of public money and how this money has been used.

Through engagement with the sector, we have identified multiple elements of accountability in local government, for example:

- councillors to their constituents

- the executive (where relevant) to the overview and scrutiny function

- the executive (where relevant) and the organisation to the audit committee

- officers to the council (through line management)

- specific statutory officers to the full council (through reporting responsibilities)

- officers to their professional bodies in relation to professional standards and conduct (where applicable)

- the council for its stewardship of public resources (through external audit)

- the council to ombudsmen / inspectors / regulators

- the council to Government departments (e.g. grant funding arrangements, the PSN Code of Connection

- the council to parliamentary select committees (as and when required)

- the council to the courts/ redress schemes

- the council to wider partnerships, bodies and authorities.

The Committee for Standards in Public Life has launched a review on accountability within public bodies: this framework will be reviewed in light of the findings of that review.

Components of the improvement and assurance framework

The key components of the improvement and assurance framework for local government are set out in the following categories, shown diagrammatically through the links below:

- Actions to contribute to assurance of local authorities, by:

- officers, not usually in public

- members and officers, sometimes but not always in public

- members and officers, in public

- other bodies, not usually in public

- Local authorities’ public accountability:

- the authority holding itself to account

- others holding the authority to account.

{kind=link}

{kind=link}

Some of these components are required by legislation (e.g. the requirement for the s151 officer to report to full council if they consider that a decision will incur unlawful expenditure). Many include a mixture of legislative requirements and best practice (e.g. ensuring appropriate governance and reviews of joint ventures and local authority trading companies). Others reflect practice which is not set down in statute but is necessary in a well-run authority. A significant proportion reflect content from the best value standards and/or reports relating to ‘failed’ councils which identify where key activities were absent or poorly performed.

More information about each component, with links to relevant guidance and improvement support, appears below. Engagement with sector support is itself a key component of the framework- whether from other authorities, regional, national and/or professional bodies - for benchmarking, sharing good practice and seeking assurance and support for improvement. All authorities – including those seeking to move from good to great – can benefit from looking outwards to learn from practice elsewhere.

The LGA’s regional teams can advise on a range of support for local authorities which will help understanding and implementation of the assurance activities shown below. This includes bespoke support and mentoring in addition to:

- councillor and officer development

- top team development

- corporate, finance and governance peer challenges

- transformation tools and support

- assurance reviews provided by CIPFA and Local Partnerships (for individual services, business cases and programmes).

In addition to considering what the key components are, read on to consider how they are implemented, with information about key principles and what good looks like.

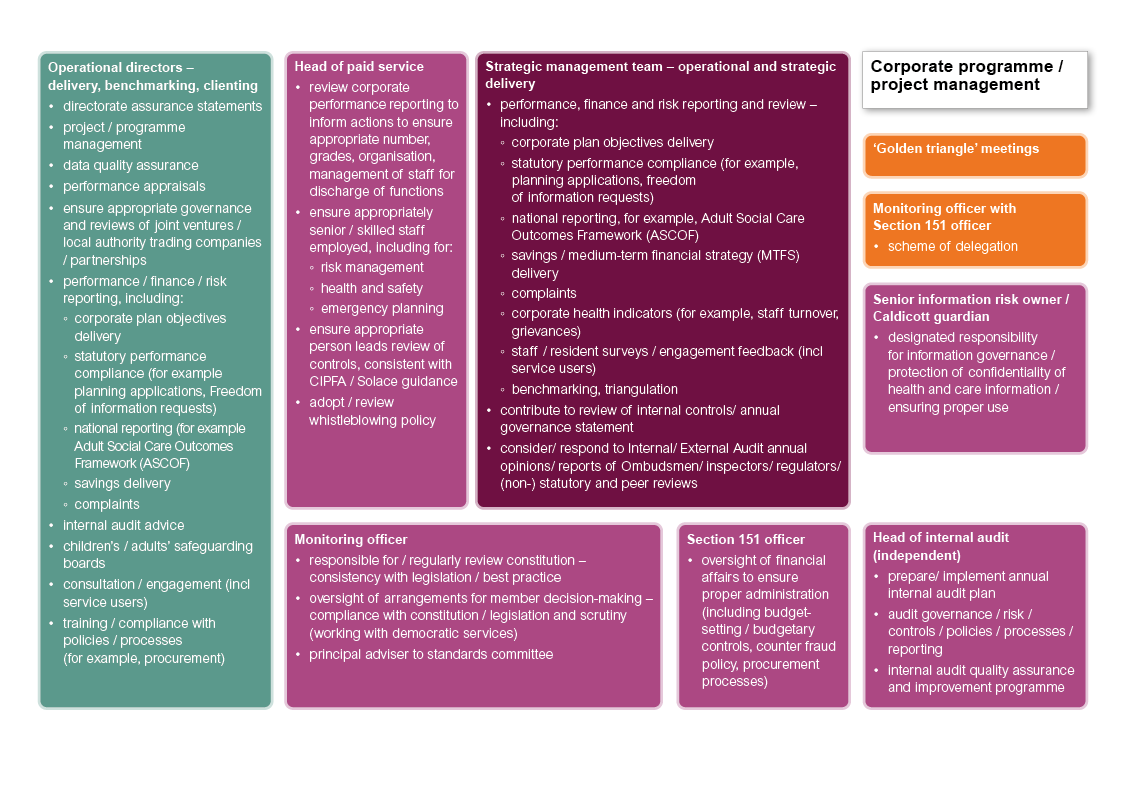

Actions to contribute to assurance of local authorities by officers (not normally in public)

Open a larger version of this diagram

{kind=link}

- Operational directors ensure that:

- directorate assurance statements to inform the annual governance statement are comprehensive and accurate, informed by an assessment of compliance with all relevant policies and procedures;

- project and programme management complies with corporate requirements and good practice;

- data used to inform decision-making and performance monitoring is of high quality. Effective performance management, using good quality data, is a necessary contribution, but is not the only source of assurance. Services where poor performance may be less visible (such as social care) require additional, and different performance management;

- performance appraisals are conducted consistently, with individual objectives linked to corporate objectives; capability and disciplinary procedures are utilised consistently and as appropriate;

- appropriate governance is in place for any partnerships, joint ventures and local authority trading companies and that it is reviewed regularly (including ensuring clarity of shareholder roles, avoiding conflicts of interest and consideration of independent data on performance);

- there is appropriate oversight of reporting on performance, finance and risk, including:

- delivery of corporate plan objectives

- compliance with statutory requirements (e.g. timescales for determination of planning applications, response to FOIs)

- national outcomes frameworks (e.g. ASCOF)

- delivery of budget savings

- responses to and learning from complaints;

- actions in response to internal audit recommendations are implemented to agreed timescales;

- effective consultation and engagement with service users and wider communities informs service design, planning and delivery. This is fundamental to accountability and requires consideration of any actions or support required to enable communities to engage with the authority;

- all necessary training is delivered to relevant members and officers to enable compliance with policies, procedures and strategies (including HR, standards, procurement and risk management). For senior member and officer roles, this should include space to reflect on practice, for example through mentoring.

- Corporate programme/ project management reflects good practice, with capacity and capability commensurate with the scale, complexity and risk of the authority’s major programmes.

- The strategic management team effectively oversees operational and strategic delivery, including:

- reporting and review of performance, finance and risk, including:

- delivery of corporate plan objectives

- compliance with statutory requirements (e.g. timescales for determination of planning applications, response to FOIs)

- national outcomes frameworks (e.g. ASCOF)

- delivery of budget savings and medium term financial strategy

- responses to and learning from complaints

- corporate health indicators (e.g. staff turnover, grievances)

- staff/ resident surveys and feedback from service user and community engagement

- benchmarking with relevant organisations

- triangulation of all sources of data on performance;

- contributing to the review of the effectiveness of the authority’s governance arrangements to inform the annual governance statement;

- considering and responding to annual reports by internal and external audit, ombudsmen, inspectors, regulators and peer reviews, and statutory/ non-statutory reviews.

- reporting and review of performance, finance and risk, including:

In addition to considering all of the above individually, it is essential that the strategic management team consider the cumulative impact where limited or no assurance is possible in relation to more than one issue or service. A trend of, for example, increasing complaints, whistleblowing and staff turnover may be an indicator of more systemic failings.

- The head of paid service:

- reviews corporate performance reporting to inform their actions to ensure the appropriate number, grades, organisation and management of staff for the discharge of the authority’s functions;

- ensures appropriately senior and skilled staff are employed, including for:

- risk management

- health and safety

- emergency planning and business continuity;

and that these arrangements are appropriately managed and coordinated;

- ensures that an appropriate person leads the review of the effectiveness of the authority’s governance arrangements to inform the annual governance statement;

- ensures adoption, effectiveness and regular review of the authority’s whistleblowing policy.

Top tips for chief executives in ensuring good governance and assurance.

- The monitoring officer:

- regularly reviews the constitution to ensure that it reflects both legislation and good practice (working with Democratic Services);

- oversees arrangements for member decision-making, ensuring their compliance with the constitution and legislation

- acts as principal adviser to the Standards Committee (the LGA has commissioned guidance and training materials to support monitoring officers in this role).

- The chief finance officer is responsible for ensuring proper administration of the authority’s financial affairs (including budget-setting, budgetary controls, procurement practices and the authority’s counter-fraud policy).

- The head of paid service, monitoring officer and chief finance officer act together as the ‘Golden Triangle’ to ensure and support good governance in the authority.

- The monitoring officer works with the chief finance officer to ensure that the authority’s scheme of delegation is regularly reviewed, appropriately comprehensive, current, and with member-level decision-making and transparency proportionate to the scale of the authority’s activity and risks.

- The Senior Information Risk Owner has responsibility for information governance and managing information security risks. In upper tier and unitary authorities, the Caldicott Guardian ensures that the confidentiality of people’s health and care information is protected and that it is used correctly.

- The head of internal audit provides independent assurance by:

- preparing the annual internal audit plan, informed by risk in the authority, and implementing that plan;

- auditing the authority’s governance, risk management, controls, policies, procedures and reporting;

- developing and implementing the internal audit quality assurance and improvement programme, including external assessment against the Public Sector Internal Audit Standards.

Actions to contribute to assurance of local authorities by members and officers working together (sometimes but not always in public)

- Officers provide professional advice which informs members’ decisions. It is essential that this advice includes all relevant information (including consideration of risk and options analysis), is current and presented in a way that is comprehensible to the decision-makers.

Where this information relates to a ‘key decision’, such information might appear in background papers which would normally be published. Authorities need systems in place to recognise where this applies and to ensure that papers are consistent and comprehensive.

Members and the public can be supported to understand the implications of the annual budget if the ‘s.25 statement’ by the chief finance officer on the council’s financial sustainability is clearly worded in non-technical language and is prominent as a separate report on the Cabinet/ Policy and Resources Committee and full council agendas.

Where a decision is required on very technical matters (for example on treasury management or certain kinds of commercial decisions), the council may need to engage industry specialists to inform decision-making (including the preparation of technical assessments).

Assurance is not a one-off activity: the advice or business case on which a decision was based may change over time. Officers have a responsibility to bring such changes, where material, to the attention of decision-makers. Where no assurance is possible due to changed circumstances, this may require consideration of additional mitigations or even the reversal of the decision.

Guidance on taking a structured and robust approach to considering commercial activity

- Each portfolio holder or policy committee chair meets regularly with directors relevant to their remit to review performance, finance and risk, consider activities required where assurance is not gained, and ensure appropriate formal reporting to members;

- The community safety partnership has oversight of the development and implementation of relevant cross-organisation strategies;

- Other boards and partnerships, such as Growth Boards or Joint Committees, are constituted to oversee activities which can only be achieved by the local authority working in partnership with others. Clear governance arrangements are essential to enable assurance of the partnership’s activity and accountability for delivery.

Less work has been undertaken to date to understand good practice in assurance of partnership activities (formal and informal) where there is shared accountability for delivery: the LGA will commission work to support a greater understanding of this topic in 2024/5.

- The authority may commission peer-led challenges for individual service areas and/or at corporate level, from the LGA (e.g. corporate peer challenge), professional bodies (eg CIPFA financial resilience advisory reports) and regional bodies. The corporate peer challenge (CPC) considers the effectiveness of the authority’s political and managerial leadership, as well as its prioritisation, culture, governance, financial management and capacity to improve: authorities are expected to publish the report and action plan and have a follow-up visit to review progress. The preparation of an honest self-assessment ahead of a CPC is an important part of the process.

- A Council Improvement Board or Independent Assurance Panel (e.g. Wirral) may provide additional focus to and assurance of the authority’s improvement activity, which may be targeted on prevention as opposed to recovery from failure.

The LGA will produce a version of this framework for elected members explaining their roles in contributing to the assurance of the authority.

Actions to contribute to assurance of local authorities by members and officers in public

- The Executive / Policy and Resources Committee reviews performance, finance and risk reporting at a strategic level, including:

- delivery of corporate plan objectives;

- compliance with statutory requirements (e.g. timescales for determination of planning applications, response to FOIs)

- national outcomes frameworks (e.g. ASCOF)

- delivery of the medium term financial strategy

- corporate health indicators (eg staff turnover, grievances).

Reporting should be regular: good practice would be at least quarterly;

- In authorities with the executive governance model and those with the committee system which choose to appoint them, overview and scrutiny committee(s):

- review performance/ finance/ risk reporting

- undertake pre-decision and/or budget scrutiny

- call-in executive decisions

- undertake scrutiny reviews in order to support policy development or consider and review strategic options.

The work of scrutiny is supported by the statutory scrutiny officer.

When reviewing finance and risk issues, scrutiny will need to have regard both to the work of the audit committee but also to the executive’s own role in oversight and assurance.

There is statutory guidance which sets out how effective overview and scrutiny should be conducted, and support and further guidance is available from the Centre for Governance and Scrutiny. For devolved areas, a scrutiny protocol provides further detail.

- The Appointments Committee recommends to full council the appointment of appropriately qualified statutory officers;

- The Audit Committee:

- monitors and reviews the effectiveness of the authority’s internal controls, risk management and financial reporting holds internal and external audit to account;

- approves the internal audit plan, ensuring that it is informed by the strategic risks facing the authority. It oversees the plan’s implementation and ensures compliance with the Public Sector Internal Audit Standards (set by CIPFA, who add interpretations for the UK public sector to international internal audit standards);

- reviews internal and external audit reports and opinions and oversees management responses;

- assesses its own practice (an annual external review is recommended)

- may include lay members to provide additional expertise.

CIPFA provides more detailed guidance, including terms of reference for Audit Committees.

The LGA provides a range of support for audit committees:

- Ten questions for audit committees to ask.

- Audit Committees: Leadership Essentials

- Regional audit forums for audit committee chairs provide an opportunity to access training, share good practice and discuss common issues. Email for more information.

The Centre for Governance and Scrutiny has produced guidance on the respective roles of audit and scrutiny committees.

- The committee with delegated responsibility for governance:

- reviews the draft annual governance statement

- oversees regular reviews of the constitution.

- The Standards Committee:

- reviews the member code of conduct and arrangements for investigating complaints into member conduct to ensure compliance with the Nolan Principles

- reviews the monitoring officer’s annual report

- seeks the perspective of the committee’s Independent Person(s).

In many authorities the committee is also responsible for overseeing the development and implementation of programmes of member training, ensuring their appropriateness and take-up by members. If this is not within the remit of Standards Committee, the authority will need to ensure that another member-level body has that remit.

The role of Standards Committee as part of the governance framework is distinct and should be separate from that of the Audit Committee which oversees the effectiveness of that framework.

- The following officers have a statutory duty to report to full council:

- The head of paid service, on arrangements for discharge of the authority’s functions (s.4 of the Local Government and Housing Act 1989)

- The chief finance officer (s.151 officer in councils and s.73 officer in combined authorities):

- on the robustness of the estimates for expenditure and adequacy of the proposed financial reserves (s.25 Local Government Act 2003)

- if there is or is likely to be unlawful expenditure or an unbalanced budget (s.114 of the Local Government Finance Act 1988)

- The monitoring officer on matters they believe to be illegal or amount to maladministration (s.5 of the Local Government and Housing Act 1989)

Before issuing a report, the chief finance officer or monitoring officer must first consult (as far as is practicable) with the head of paid service and each other.

- Full Council is the body charged with the governance of the council and while it may delegate some responsibilities it remains accountable and therefore should seek assurance. It does this by:

- Considering the s.25 statement of the chief finance officer of the robustness of estimates and adequacy of reserves before approving the budget;

- Reviewing (at least) an annual report from each of the chairs of the Overview and Scrutiny Committee (where relevant), Audit and Standards Committees and holding them to account;

- Appointing appropriately qualified statutory officers.

Consideration of the external auditor’s annual report would also represent good practice.

Actions to contribute to assurance of local authorities by other bodies (not usually in public)

- Grant funding bodies place many and varied reporting requirements in relation to their programmes, including where the local authority is the accountable body for other agencies and wider partnerships;

- Regional networks may undertake benchmarking and maintain an overview of performance, providing constructive challenge and in some cases improvement support (e.g. London’s Self Improvement Board)

- Officials from the Department of Levelling Up, Housing and Communities (DLUHC) undertake early engagement with local authorities where they become aware of qualitative or quantitative indicators of potential failure, to understand their organisational challenges in relation to governance, finance and service delivery and to gain assurance of how they are being managed. Best Value Standards and Intervention: a statutory guide for best value authorities (section 5)

- The Office for Local Government (Oflog) will conduct ‘early warning conversations’: discussions with local authorities identified as potentially at risk. Where the initial conversation is deemed to provide insufficient assurance, the authority will be visited by a team of reviewers who will then set out their findings and recommendations in a published report.

- Government departments make ad hoc requests for information and assurance where they have queries or concerns relating to local authority performance relevant to their remit.

- Political parties have their own disciplinary processes in relation to the conduct of members of their parties – including elected members:

The parties also have their own approaches to engagement with authorities where they are the largest party and where significant performance issues have been identified.

- Local -or external – audit undertakes assurance activity throughout the year and acts as a critical friend.

- Professional bodies have varying roles in relation to standard setting, the specification and awarding of qualifications, capability and disciplinary procedures and guidance and tools to support decision making. In relation to corporate service areas, the following bodies have key roles:

| Finance |

The chief finance officer in England must be a member of one of the following bodies:

|

| Internal Audit | |

| Legal services |

There is no requirement for a monitoring officer to be legally qualified. For those that are, the following bodies are relevant:

|

- The LGA maintains an overview of the performance of the sector.

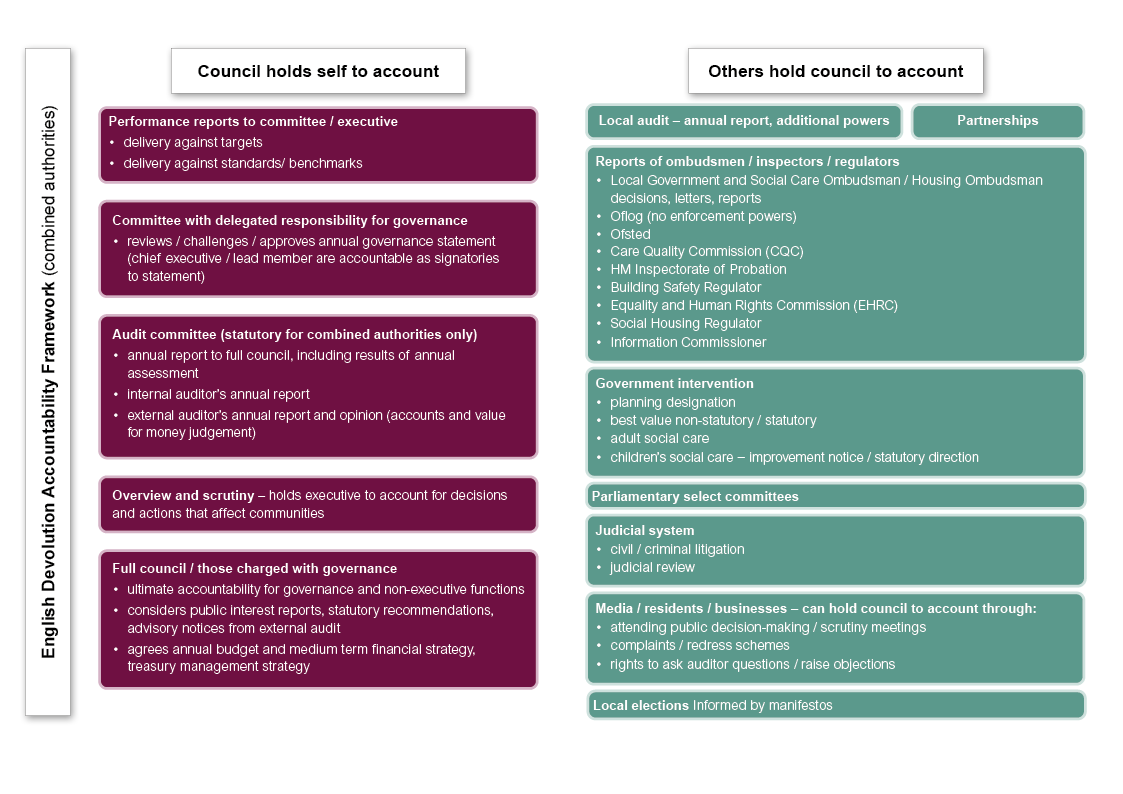

How does the authority hold itself to account?

Open a larger version of this diagram

{kind=link}

- The English Devolution Accountability Framework sets out how devolved areas are scrutinised and held to account through local scrutiny, by the public and by government.

Good governance for combined authorities

- The Executive/ Policy and Resources Committee holds itself to account for delivery against performance targets, standards and benchmarks;

- In authorities with the executive governance model, overview and scrutiny committees hold the Executive to account for the decisions and actions that affect local communities;

- The Audit Committee:

- holds management to account in relation to the opinions of internal and external audit and for the implementation of their recommendations

- is held to account by Full Council through an annual report, which should include reference to a self-assessment of its own performance;

- The committee with delegated responsibility for governance reviews, challenges and approves the annual governance statement and holds management (via the chief executive and lead member as signatories) to account for implementation of improvement actions identified;

- The Full Council:

- is ultimately accountable for the council’s governance and other non-executive functions

- considers and must ensure appropriate responses to public interest reports, statutory recommendations and advisory notices from external audit

- agrees the annual budget, medium term financial strategy and treasury management strategy.

How do others hold the authority to account?

- Ombudsmen, inspectors, regulators and others issue reports which require the authority to take action. While most of these (and the more formal interventions which follow) relate to specific services, a failure leading to an adverse judgement by one of these bodies is a probable indicator of wider failings in assurance:

- Building Safety Regulator*

- Care Quality Commission*

- Equality and Human Rights Commission*

- HMI Probation

- Housing Ombudsman*

- Information Commissioner*

- Local Government and Social Care Ombudsman

- Ofsted*

- Regulator of Social Housing

*Body with powers to take or trigger enforcement action;

Where there are services with a greater degree of regulation – often those with the largest budgets – this may skew assurance activity and attention. It is important for authorities – and particularly the chief executive – to understand the scale and nature of assurance (both internal and external) of all higher-risk services and to put additional measures in place where necessary.

There is guidance for members and chief executives to help them understand their roles in relation to the assurance of children’s services:

- Chief executives 'must know' for children’s services

- Must know: The role of a council leader in improving outcomes for children

- 'Must knows' for children's services portfolio holders

- Government departments formally intervene by issuing directions (statutory interventions) or requests (non-statutory interventions):

- A parliamentary select committee may require a local authority to appear in front of it in relation to concerns about its performance;

- The judicial system may hold a local authority to account, whether through criminal or civil litigation, or judicial review;

- Local residents and business and the media can hold their local authority to account by:

- attending public decision-making and scrutiny meetings, asking questions where permitted by the constitution

- making use of complaints or redress schemes

- invoking rights to ask the auditor questions and/or raise objections;

- Local residents hold elected members to account at local elections.

The ‘three lines’ model

The ‘three lines model’ outlines the different contributions that different sources of assurance can provide:

| First line |

Actions by managers and staff who are responsible for identifying and managing risk as part of their day to day management and delivery of services. This includes:

|

| Second line |

The way the authority oversees the effectiveness of its controls so that it operates effectively, for example, the responsibilities of:

|

| Third line | Independent assurance, i.e. internal audit. Accountable to full council. |

| Governing body | Full council |

| External assurance providers |

For example:

|

There should be regular dialogue and coordination between the different ‘lines’ and escalation where appropriate. Regular interaction between internal audit and management will ensure the work of internal audit is relevant and aligned with the authority’s strategic and operational needs. Collaboration between the first and second lines and with internal audit will ensure no unnecessary duplication, overlap or gaps. Regular liaison between internal and external audit can inform the identification of risks. A briefing by the Institute of Internal Auditors provides more detail on how the different sources should complement each other.

Key principles of good assurance and accountability

- Clarity: understand who is accountable for what. Is it easy to see in your council’s constitution who can take which decisions? Do the people who have key roles relating to assurance in your council have a shared understanding of those roles and have they had appropriate training?

- Proportionality: assurance activity must add value, be cost-effective and be proportionate to the level of risk. As risk changes, so should the council’s assurance activities, both at a strategic level and in relation to specific high-risk activities.

The governance risk and resilience framework provides a tool for authorities to identify, understand and act on risks to good governance. The Centre for Governance and Scrutiny have also provided a briefing on the respective roles of audit and scrutiny in the oversight of risk.

ALARM provides training and guidance to public sector risk management professionals in the UK.

- A whole-council approach: assurance isn’t just the responsibility of the Monitoring Officer or the Head of Internal Audit. All members have a responsibility to oversee effective governance, and all officers have a duty to comply with good governance and provide information to demonstrate that compliance. Everyone should understand their contribution – and this may include partners and other stakeholders.

The opportunity provided by the preparation of the annual governance statement to step back and consider how well the authority’s systems and controls are working as a whole is a crucial one: depending on the scale of challenges and risks the authority is facing, the corporate statutory officers and/or audit committee may need to find other opportunities to do so at intervals during the year.

- A culture of assurance and accountability, with a low tolerance for poor governance/ performance. ‘The culture of any organisation is shaped by the worst behaviour the leader is willing to tolerate’ (School culture rewired, Gruenert and Whitaker). Councils which entered statutory intervention had many of the right processes in place, but cultures which tolerated non-compliance, including poor behaviours. In some places there was a lack of curiosity and intolerance of internal challenge to norms: while trust is important, so is constructive challenge.

The existence of a policy or procedure does not in itself provide assurance: is there sufficient evidence to show that it is appropriately and consistently implemented?

- Monitoring against standards, benchmarks and local targets: some elements of what good performance looks like change over time: understanding how the authority performs in terms of value for money should be a constant endeavour. In addition to local targets, many council service areas will have standards against which they are measured: reporting to elected members should include performance against these. LG Inform is freely available to all and enables any council’s performance to be compared with any other council or group of councils.

- Credible, quality data and information: elected members and the public can only be assured where they are confident in the quality of the information on which assurance judgements are based.

The Better use of data programme supports local authorities to develop an evidence-informed culture which will enable well-informed decisions and improve service design, accountability and transparency.

- Transparency, accessibility and intelligibility of information: a commitment to transparency is a fundamental element of good governance. That commitment is hollow if key information is full of jargon or technical detail which is unintelligible to non-experts, or if it is hidden away in an obscure part of the council website.

Is confidential or ‘exempt’ information in member reports kept to an absolute minimum so that members of the public can see and understand why members are making the decisions that they do? Is there regular financial reporting to Cabinet/ Policy and Resources Committee during the year? Is the information that enables, for example, audit committee to be assured easily accessible?

Access to information for elected members.

- Seeking and engaging with external challenge and support: There are multiple opportunities for peer challenge and support at (sub)regional and national levels, for individual services and at a corporate level.

- Independent assurance: assurance should be proactively sought from a variety of sources. All of the corporate statutory officers, in particular, should be prepared to approach audit (whether internal or external, both are independent) with any concerns and seek their advice, in addition to commissioning audits of specific activities or programmes. Where risks are significant, the council should consider seeking additional external assurance from relevant experts.

What does ‘good’ look like?

Good practice in local government assurance includes:

- Visible, collective ownership and leadership of good governance by both political and managerial leaders. All members and officers should be able to see that the council’s political and managerial leadership prioritise assurance activity and accountability. This includes taking difficult decisions as and when necessary.

Top tips for chief executives on governance and assurance are designed to support chief executives to keep at ‘front of mind’ the key elements of good governance and assurance. The chief executives’ development hub provides support for the complex set of accountabilities that chief executives hold.

We will soon be publishing similar tips for elected mayors and leaders. The Leadership Academy and Leadership Essentials support the development of political leadership skills.

- Being a learning organisation. Continuous improvement requires continual learning and development. Self-awareness is an essential first step, with a recognition of both strengths and areas for development. Organisations which guard against complacency are less likely to be caught by ‘unknown unknowns’. Openness to external challenge and a lack of defensiveness are also prerequisites.

Continuing professional development is essential for both corporate statutory officers and the authority’s political leadership.

- Assurance as a constant process, not a one-off event. The external auditor’s annual report mainly looks back at previous activity, and internal audit reports capture practice at a moment in time. Ensuring consistent use of processes and engagement with training, and use of monitoring information can help provide assurance between bigger assurance ‘events’.

- Assurance supports the achievement of priority outcomes. Assurance is not an end in itself. A culture of assurance and accountability is more likely to be embedded where elected members and officers understand that assurance activity keeps the council ‘safe’ and able to deliver for residents.

- Making it easy for the public to hold the council to account. This includes communicating well with the public on the council’s performance and ensuring public understanding of and access to key accountability opportunities and assurance information. In addition to meaningful compliance with the Transparency Code, this would include, for example, making it easy for the public to access:

- a two-page summary of the budget

- the annual governance statement (or a summary) and action plan

- the external auditor’s annual opinion letter and in particular the value for money judgement

- corporate performance reports which show the council’s performance in relation to others (potentially using LG Inform)

- reports from peer challenges and regulators, with associated action plans

- a comprehensive forward plan which shows what decisions will be made by members in the coming months

- equality impact assessments related to member decisions and other information related to the Public Sector Equality Duty

-

information provided in response to freedom of information and environmental information requests.

It is important to recognise that in many places, the local media does not cover local government in the same depth or detail as was previously the case. The development of social media has also had impacts on behaviour, defensiveness and openness in some places. The council’s communications team has an important role to play in ensuring that the council’s commitment to transparency is reflected in practice and building relationships with local media and local democracy reporters to help them understand key performance and assurance information.

The LGA will produce a version of this framework explaining how the public can contribute to holding their local authority to account.

We have collected some case studies which give examples of recent good practice in councils.